GLP-1 prescriptions for weight loss climb sharply, despite persistent barriers

Key Takeaways:

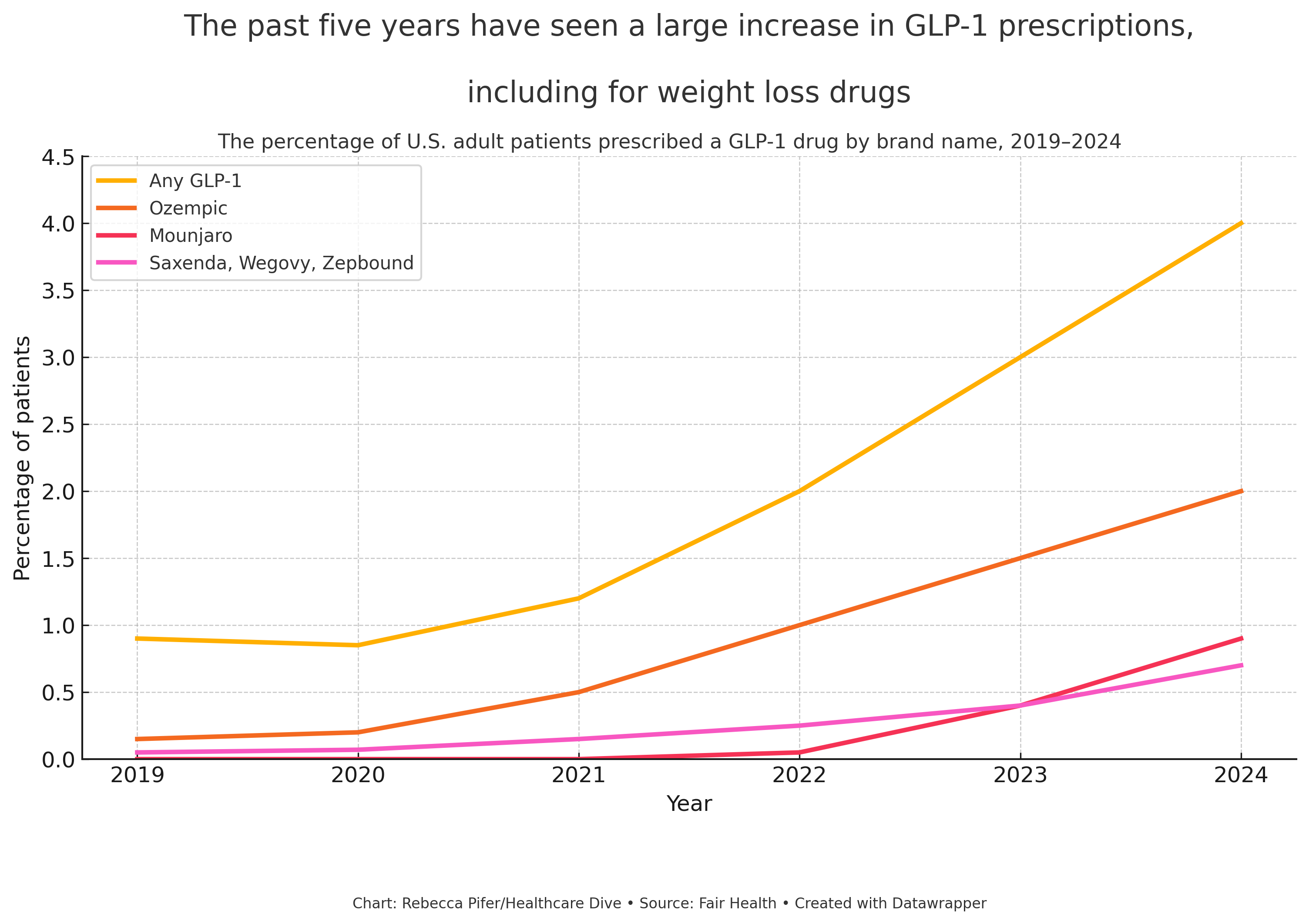

- GLP-1 prescriptions for weight loss have increased by nearly 2,000% among people without diabetes between 2019 and 2024, according to Fair Health data.

- Drugmakers face criticism and logistical challenges, including high costs, shortages, and concerns about replacing behavioural and surgical interventions.

- Government resistance to subsidising obesity medications and rising public scrutiny may slow broader uptake, despite clinical success and commercial demand.

Background: GLP-1 Receptor Agonists and Rising Obesity Treatment Demand

Glucagon-like peptide-1 receptor agonists (GLP-1 RAs) are a class of drugs that simulate a gut-derived hormone responsible for lowering blood glucose levels and suppressing appetite. Initially approved for the treatment of type 2 diabetes, these medications have more recently demonstrated efficacy in supporting weight loss. Their expansion into the field of obesity care has transformed both patient outcomes and the commercial pharmaceutical landscape.

Fair Health, a U.S.-based non-profit organisation, analysed over 51 billion commercial claims to identify trends related to GLP-1 prescriptions and obesity care. The data show a significant rise in GLP-1 prescriptions, particularly for weight loss purposes rather than diabetes management.

Explosive Uptake in Weight Loss Prescriptions

Among individuals prescribed GLP-1 medications in the past year, approximately half received the prescription for weight management, not for diabetes. When people living with type 2 diabetes were excluded from the dataset, the data revealed a 1,961% increase between 2019 and 2024 in prescriptions to individuals with overweight or obesity but without diabetes.

This staggering growth reflects both public demand and shifting clinical practice. GLP-1 RAs are increasingly viewed not only as antidiabetic medications, but as a frontline treatment option for obesity—a chronic and often intractable condition.

An Expanding Market and the Role of Industry

The commercial implications have been profound. Industry analysts project the anti-obesity drug market could exceed $100 billion globally by 2030. At present, three GLP-1 drugs are approved by the U.S. Food and Drug Administration (FDA) specifically for weight management:

- Saxenda (liraglutide) – Novo Nordisk

- Wegovy (semaglutide) – Novo Nordisk

- Zepbound (tirzepatide) – Eli Lilly

Although Saxenda received approval in 2014, it was not until Wegovy’s launch in 2021 that the weight loss potential of GLP-1s gained widespread public attention. Eli Lilly’s Zepbound followed and quickly contributed to $4.9 billion in sales in its first full year. In 2023, Novo Nordisk reported $9.9 billion in combined sales from Saxenda and Wegovy.

Shortages, Substitutes, and Setbacks

Rapid uptake led to supply shortages, during which telehealth companies partnered with compounding pharmacies to distribute non-branded formulations. Although these shortages have since resolved—restoring market exclusivity to the original manufacturers—the episode dented both projected 2025 revenues and investor confidence. It also contributed to leadership changes at Novo Nordisk.

Affordability and Access Barriers

The high cost of GLP-1 drugs remains a critical issue, with monthly list prices reported as follows:

- Wegovy: $1,350

- Zepbound: $1,060

(Source: Institute for Clinical and Economic Review)

Because long-term use is generally required to maintain weight loss, the financial burden on health plans is substantial. In 2024, fewer than 20% of employer-sponsored insurance plans covered GLP-1s for weight loss, largely due to cost constraints.

To address this, manufacturers have sought partnerships with major pharmacy benefit managers. Recent collaborations include:

- Novo Nordisk and Eli Lilly with Cigna’s health services subsidiary to offer discounts and cap out-of-pocket costs

- Novo Nordisk with CVS Caremark, granting Wegovy preferred formulary status

Policy Resistance and Political Backdrop

Obesity remains a public health emergency in the United States. According to the Centers for Disease Control and Prevention (CDC), over 40% of adults are currently living with obesity, a figure projected to reach 50% by 2030. Yet federal support for pharmacological obesity treatment remains limited.

Earlier this year, the Trump administration rejected a proposal to expand Medicare coverage to include anti-obesity drugs, a move that would have added $40 billion to taxpayer expenditures over ten years.

The decision coincides with political and cultural scrutiny of pharmaceutical interventions. Health and Human Services Secretary Robert F. Kennedy Jr. has been vocal in his opposition to pharmacological weight loss treatments, attributing rising obesity rates to poor dietary choices. He has argued that medication should not replace healthier food and lifestyle interventions.

“We cannot medicate our way out of a nutrition crisis,” Kennedy stated in a White House report released last week.

Impact on Other Forms of Obesity Care

Fair Health’s findings suggest that the rise in GLP-1 prescribing has coincided with a decline in bariatric surgery rates. This supports prior research indicating that patients are increasingly turning to pharmacotherapy instead of more invasive interventions.

However, the trend has also been linked to a reduction in behavioural health interventions, which raises significant clinical concerns. GLP-1s have been associated with increased risks of depression, anxiety, and suicidal ideation in some individuals, making ongoing psychological support an essential component of care.

Looking Ahead

While new partnerships and forthcoming price negotiations under the U.S. Inflation Reduction Act (effective 2027) may improve affordability—particularly for Medicare recipients—current dynamics underscore the complex interplay of clinical promise, economic burden, and political ideology.The rapid growth of GLP-1 prescribing marks a new chapter in the treatment of obesity. Yet its future success will depend not only on drug efficacy, but also on ensuring equitable access, maintaining comprehensive care, and fostering public trust in what remains a deeply politicised health issue.